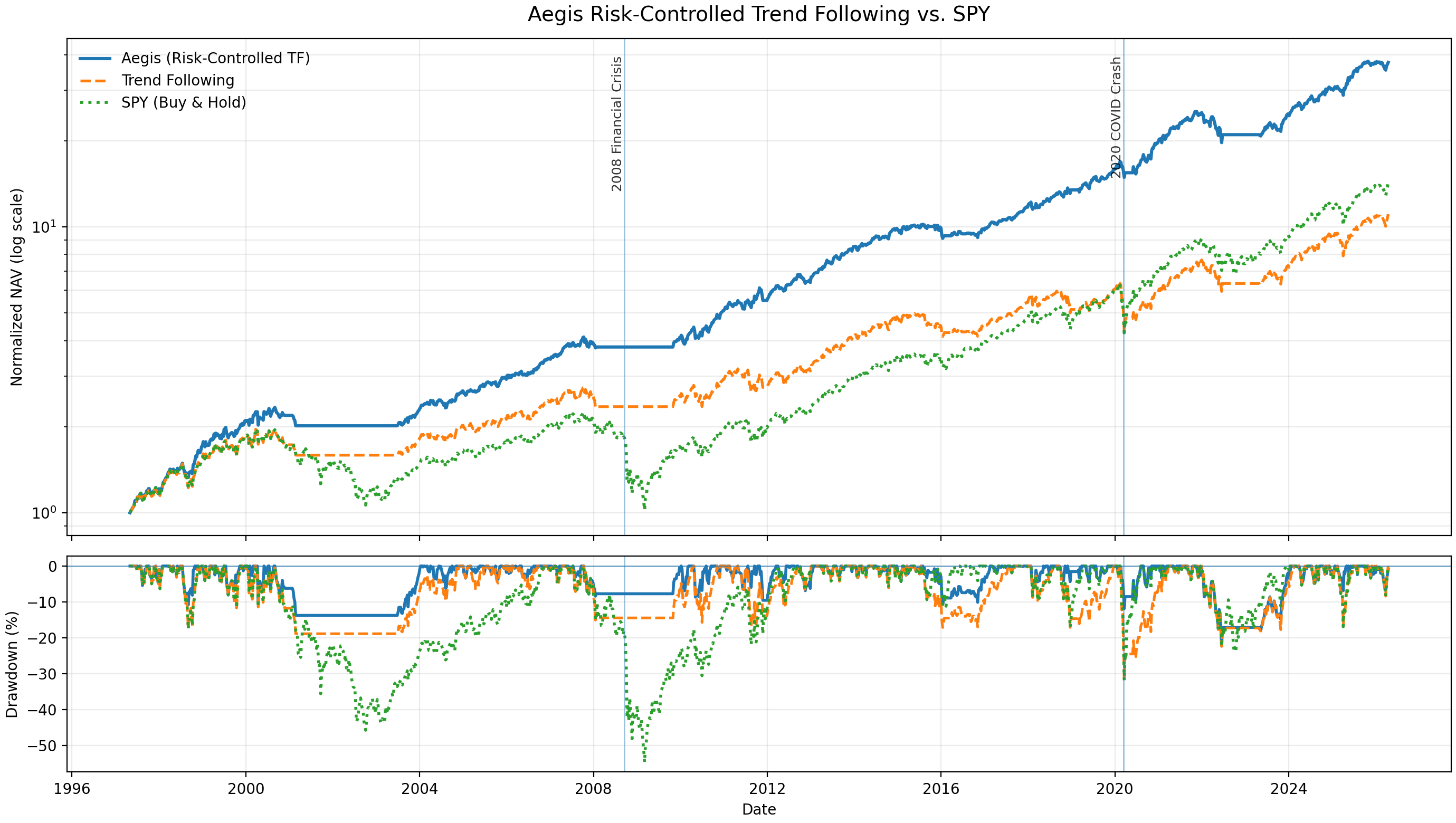

Aegis dynamically controls exposure using VPI, achieving consistently superior risk-adjusted performance with significantly reduced drawdowns.

Ongoing Research: Fokker–Planck Framework

A preliminary visualization of an ongoing research framework. The four-panel structure captures the interaction between volatility dynamics, state evolution, and adaptive risk response.

What is VPI?

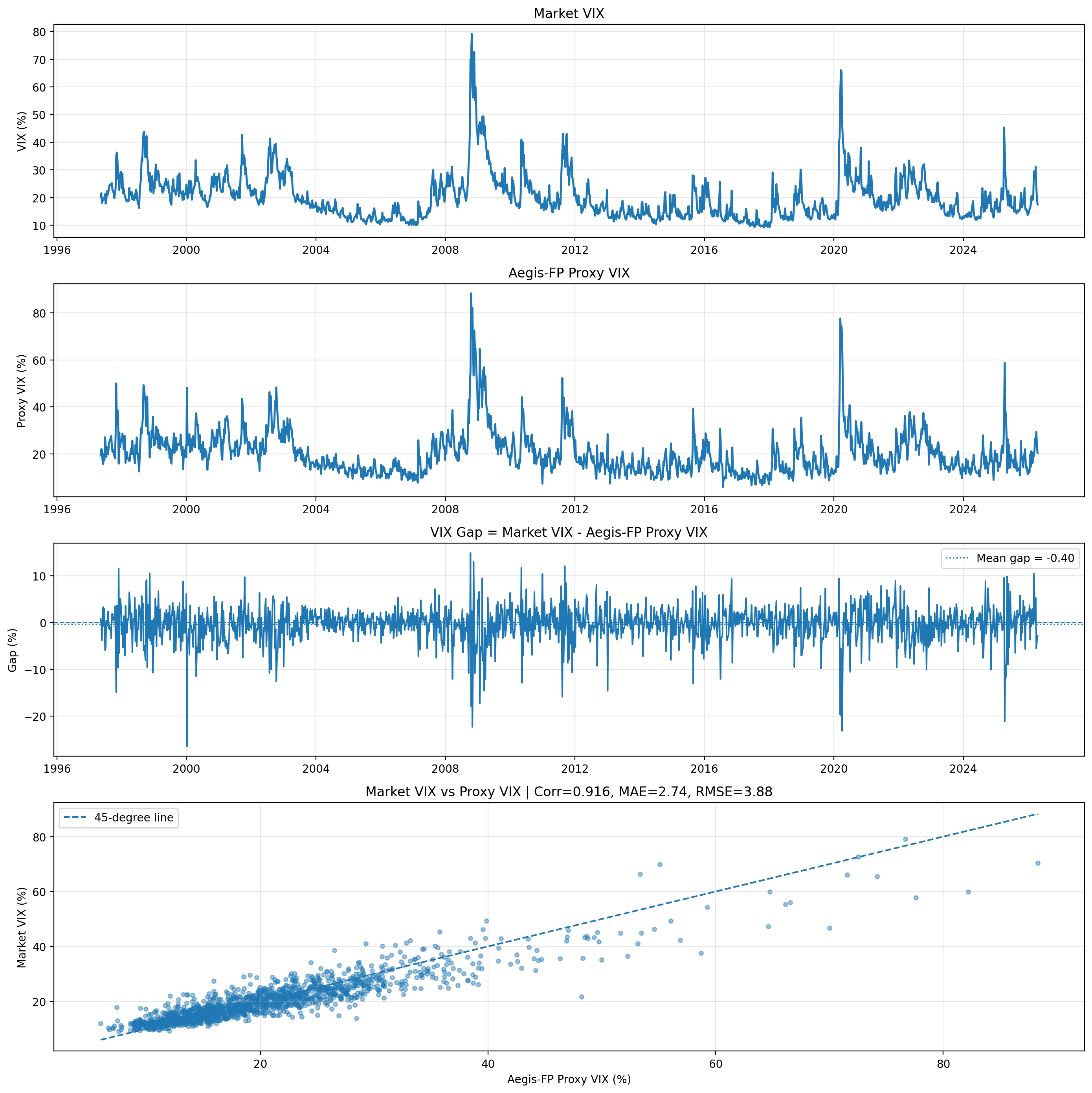

The Volatility Pressure Index (VPI) measures the dynamic change in variance, capturing the directional pressure of volatility in financial markets.

Rather than focusing only on the level of volatility, VPI highlights how volatility evolves and where structural stress begins to build.

Working Paper

A Fokker–Planck Framework for Variance Dynamics:

Structural Reconstruction and Decomposition of Implied Volatility

A State-Space Approach to Variance Dynamics

Toshiharu Honda

Quant Finance Lab Kagoshima

June 2026

Aegis: A Dynamic Risk Control Framework Based on the Volatility Pressure Index (VPI)

A Simple Law of Variance Dynamics

Toshiharu Honda

Quant Finance Lab Kagoshima

April 2026