Aegis: A Dynamic Risk Control Framework

Based on the Volatility Pressure Index (VPI)

A framework that reduces drawdowns while maintaining market participation.

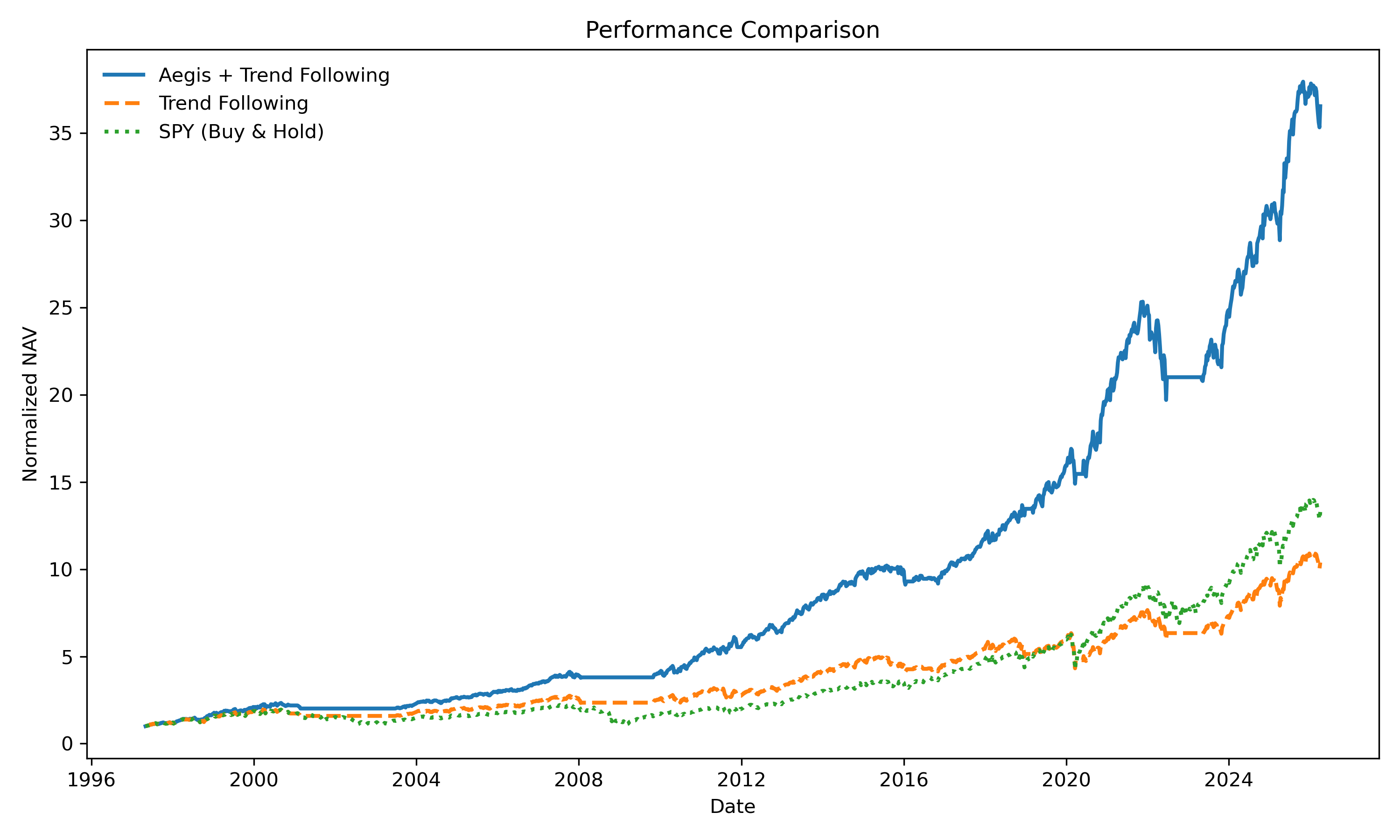

Long-term performance comparison of Aegis + Trend Following, Trend Following, and SPY.

Abstract

We introduce the Volatility Pressure Index (VPI), defined as the logarithmic change in variance.

VPI captures the dynamics of volatility as a cumulative state variable rather than a static level.

Based on this framework, we propose Aegis, a dynamic risk control system that continuously adjusts market exposure.

A forward test on SPY shows that Aegis reduces drawdowns while improving risk-adjusted returns.

This study provides a new perspective on volatility as a dynamic process described by state and change.

Current Regime

MPAM Status: cash_replaced_by_SHY_state_harbor

SPY

Status: normal

Exposure: 20%

EWJ

Status: reentry

Exposure: 20%

VGK

Status: reentry

Exposure: 20%

EEM

Status: reentry

Exposure: 20%

DIA

Status: normal

Exposure: 20%

TLT

Status: normal

Exposure: 0%

GLD

Status: reentry

Exposure: 0%

FTGC

Status: reentry

Exposure: 0%

SHY

Status: active

Exposure: 0%

Last Update: 2026-07-08

SPY

Status: normal

Exposure: 20%

EWJ

Status: reentry

Exposure: 20%

VGK

Status: reentry

Exposure: 20%

EEM

Status: reentry

Exposure: 20%

DIA

Status: normal

Exposure: 20%

TLT

Status: normal

Exposure: 0%

GLD

Status: reentry

Exposure: 0%

FTGC

Status: reentry

Exposure: 0%

SHY

Status: active

Exposure: 0%

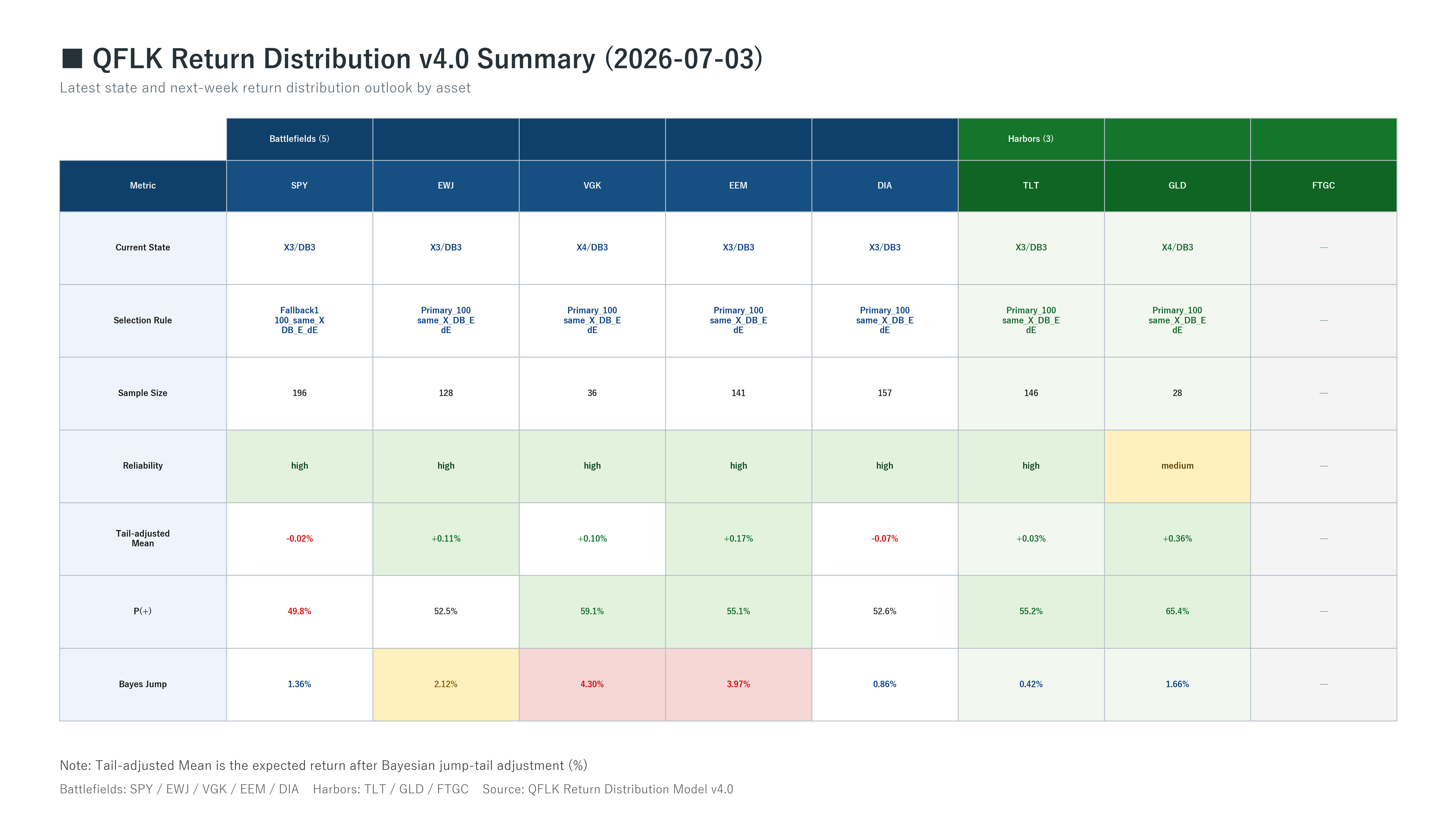

QFLK Return Distribution v4.0

Tail-adjusted Mean is the expected return after Bayesian jump-tail adjustment (%).

Battlefields: SPY / EWJ / VGK / EEM / DIA

Harbors: TLT / GLD / FTGC

Battlefields: SPY / EWJ / VGK / EEM / DIA

Harbors: TLT / GLD / FTGC

Last Update: 2026-07-08

Operational Updates